Continental Coal Ltd has rapidly shifted from being a junior player in the coal exploration market to achieving profitability as a mid-tier producer. CEO Don Turvey talks to Jayne Alverca.

The journey from exploration to production is fraught with danger. For many junior entrants, initial high hopes quickly founder in a mire of bureaucratic wrangling over licenses and permits; or the difficulties of raising finance; or the unpalatable realisation that the glittering prize in question simply cannot be extracted at a profit. It is an industry where optimism can easily turn to ashes and countless once-promising discoveries have led nowhere.

CEO of Continental Coal Don Turvey joined the company last year and possesses a deep knowledge of African exploration and mining operations. He has overseen the company’s emergence as a mid-tier player, a transition that has taken place with remarkable success and also at great speed. “Over the past 18 months we have undergone a transformation from an exploration company to become an established mid-tier mining company with two very productive thermal coal mines in operation, two others under development and a very strong base in South Africa. We have clearly proved our ability to deliver exceptional operational results and convert prospects into productive mines,” he states.

In September 2011, Continental shares became available on the London AIM Exchange, a listingintended to complement existing listings on the ASX and US OTCQX. International exchanges achieve a higher international profile for the company by aligning it with the investment mandate of a wider group of investors, particularly institutional investors.

“The listing of its securities on AIM—recognised as one of the world’s leading resources-focused equities exchanges—is very strategic for Continental Coal,” Turvey continues. “The listing was not intended to raise capital as we are already fully funded for our third mine development. Rather, we wanted to diversify our investor base. Before, it was very difficult for investors in the UK, Europe and the US to become involved. Now we believe our investor base will gradually shift towards these areas.”

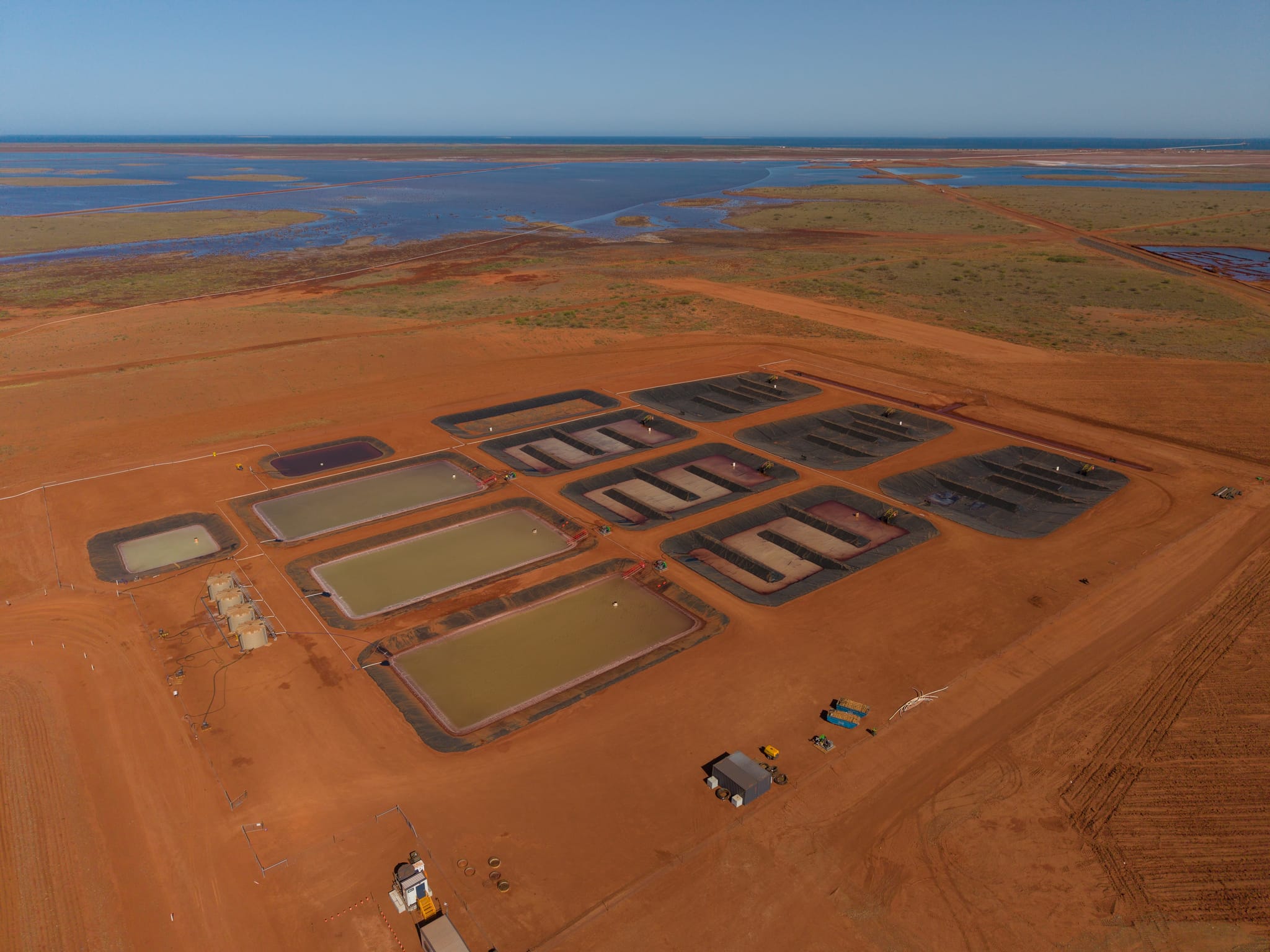

The investment press has shown great excitement over the potential production capability of Continental’s holdings. At present, there are two operating mines, Vlakvarkfontein and Ferreira. Between them, these two mines produce approximately two million tonnes per annum of thermal coal for both export and domestic markets. Construction work commenced to bring the third coal mine into production; and the fourth mine BFS is being reviewed. By the end of 2013, it is estimated that Continental will have achieved an annual production rate of seven million tonnes, a target that Turvey is confident will be met.

All are located in the established Central Basincoalfields area of Witbank, Highveld and Ermelo, which is South Africa'slargest coal mining area with a highly developed infrastructure and plenty of local mining expertise. “Extracting coal from these areas is a very straightforward process with a focus on open-cast and bord and pillar underground operations,” Turvey explains. “There is nothing extraordinary about our methods and we can apply standard, proven mining methodologies. This method of coal production means that we have a very low-risk profile.”

To date, production plans have centred on South Africa, but Turvey is keen to point out that the company already has interests further afield. A two-phase, 60-hole exploratory drilling programme is underway in Botswana where Continental has secured three tenements covering 964 square kilometres. Openings have also been identified in Kenya, Tanzania and Mozambique, which have both thermal coal and coking coal prospects. “Adding coking coal to our portfolio is a definite intention in the future and we will also consider opportunities outside of the continent,” he states.

Turvey believes that Continental’s success has been facilitated by a series of carefully chosen strategic partnerships which also provide a solid base for future growth. For example, the company has signed strategic offtake and funding agreements with EDF Trading for its more profitable, export thermal coal production which is expected to undergo a rapid ramp-up over the next 12 months. EDF is the leader in the international wholesale energy market with a proven capability to source, supply, transport, and store, blend and convert physical commodities across the wholesale energy markets.

Another strategic alliance earlier this year resulted in US$65 million in funding secured with ABSA Capital for the development of the Penumbra mine, where initial civil and construction earthworks have already started. ABSA Capital is a division of ABSA Bank Limited and is mandated within the Barclays Group to lead corporate and investment banking activity in Sub-Saharan Africa.

“The fact that we received two very attractive financing offers for this mine is testament to the quality of the feasibility studies we conducted and the subsequent mine development plan we approved. This finance package optimised our ongoing funding arrangements and has proved that as an emerging coal producer we are able to raise debt at attractive levels for our aggressive growth plans,” Turvey comments.

Another recent development is a joint development agreement with KORES, Korea’s state mining and exploration company. This partnership will enable the fast-tracking of the Vlakplaats coal development project, located 80 kilometres east of Johannesburg and 25 kilometres south-west of Continental’s Vlakvarkfontein mine. Under the terms of the agreement, KORES will be responsible for the offtake and marketing of export thermal coal from the project upon a decision to mine.

“Each party has gone through a very rigorous process of scrutiny before choosing to work in partnership with us. These agreements demonstrate to the markets that we are committed to the highest standards of governance and management,” he declares.

Meanwhile, Turvey looks forward to achieving a turnover next year of between $50 million and $70 million from the portfolio of holdings. In 2013, he predicts that this figure may double. “These might be tough times from a world economic perspective, but we are in an enviable cash positive position and will continue to do what we excel at, which is getting coal out of the ground and serving our customers,” he concludes. www.conticoal.com

EMEA-Nov11-B1-Continental.Coal-Bro-s.pdf

EMEA-Nov11-B1-Continental.Coal-Bro-s.pdf